Payroll tax issues for Medical Centre business arrangements

Recent events highlighted in “Accountants Daily” by Matthew McKee of Brown Wright Stein Lawyers, has changed the understanding and treatment of some aspects of medical centre operations.

A recent ruling in the Victorian Court of Appeal against The Optical Superstore means that all medical and related practices should review their payroll tax obligations.

If your practice uses a tenancy/agency model, this could impact you.

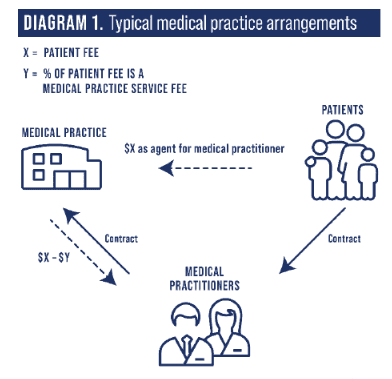

What is the tenancy/agency model?

This is one of the most common business arrangements used in the medical industry, whereby the practice collects the fees from the patient, deducts a fee from these amounts for providing the management service (usually to cover rent, administration staff, marketing, practice supplies etc) and then pays the remainder to the actual medical practitioner.

The payments by the practice to the medical professional are commonly treated as fees or revenue earned by the individual, rather than wages.

This is because money being paid to the medical professional was considered theirs already and was simply being held by the practice on trust - in a similar fashion that they would have received their remuneration, if they had been running their own practice.

What is wrong with this arrangement?

In Commissioner of State Revenue v The Optical Superstore Pty Ltd [2019] VSCA 197, it was determined that these payments could be subject to payroll tax.

If your practice uses this structure, you could be required to include the payments made to the individual medical professional as wages instead of contract income, and subsequently pay payroll tax.

If that is the case, you may also be required to pay, in addition to the unpaid tax for the past five years, up to 25 per cent of the taxed owed for the past five years as a penalty and interest.

What happened in this case?

The case was between Victoria’s Office of State Revenue and The Optical Superstore. The Optical Superstore has more than 65 stores across Australia selling eyewear and optometry services.

The optometrist treated patients inside a consulting room at a store.

The fees, whether they were paid by the patient or Medicare were put (at the optometrist’s direction) into The Optical Superstore’s main operating bank account. The fees were held “on trust” for the optometrist but, importantly, were not held in any form of separate or sub-account.

Each month, The Optical Superstore paid the optometrist a “reimbursement amount” based on the hours worked by the optometrist.

Each optometrist would submit their hours to the store manager for sign off. Then payment would be made to the optometrist.

The optometrists were not providing invoices to The Optical Superstore.

An “occupancy fee” was deducted from each optometrist’s payment equal to the gross consultation fees (what the patient actually paid) less what was paid to the optometrist (patient fee = “occupancy fee” + “reimbursement amount”).

If the gross consultation fees were less than the amount that the optometrist was entitled to, based upon their hourly rates, the difference was treated as a “location attendance premium” (GST would be paid and a recipient created tax invoice issued).

What made The Optical Superstore case so special?

What is not usually seen in a medical practice structure is:

The optometrist’s fees were based on hours worked — like a “normal” employee wage structure.

The “location attendance” premium.

The optometrist’s effective time sheet was signed off by the store manager (like a “normal” employee).

The Optical Superstore was also selling products in conjunction with the optometry services.

The Victorian Commissioner considered the agreement between the optometrists and The Optical Superstore a “relevant contract” for work according to the laws around payroll tax.

This meant that the payments made to the optometrists should be treated as wages from a tax perspective and therefore grouped together across the stores and subject to payroll tax.

Not all Medical Centre arrangements are the same

The Optical Superstore had special features such as the location attendance premium and the sale of products with services. This is not always the case with more traditional structures. What is of concern is that the judge in the Supreme Court of Victoria adopted a broad view of what constituted a contract for work.

This means that these types of structures could be reviewed in the future and with over 90 per cent of state payroll tax investigations identifying some level of non-compliance, we may need to review the potential risk.

If you believe that your business structuring may need a review with regard to the many levels of taxation being imposed today, please do not hesitate to contact us, so we can look at your situation more specifically.

As always, if you have any other concerns or queries in relation to this or any other financial matter, please do not hesitate to contact one of the Cordner Advisory team on (07) 5504 5700 so we can discuss the matter and solutions with you.

Cordner Advisory - Your Business Advisory, Accounting & Tax Specialists. Catering for clients all across Australia, from the golden beaches of the Gold Coast and Sunshine Coast to the capital cities such as Brisbane, Sydney and Melbourne